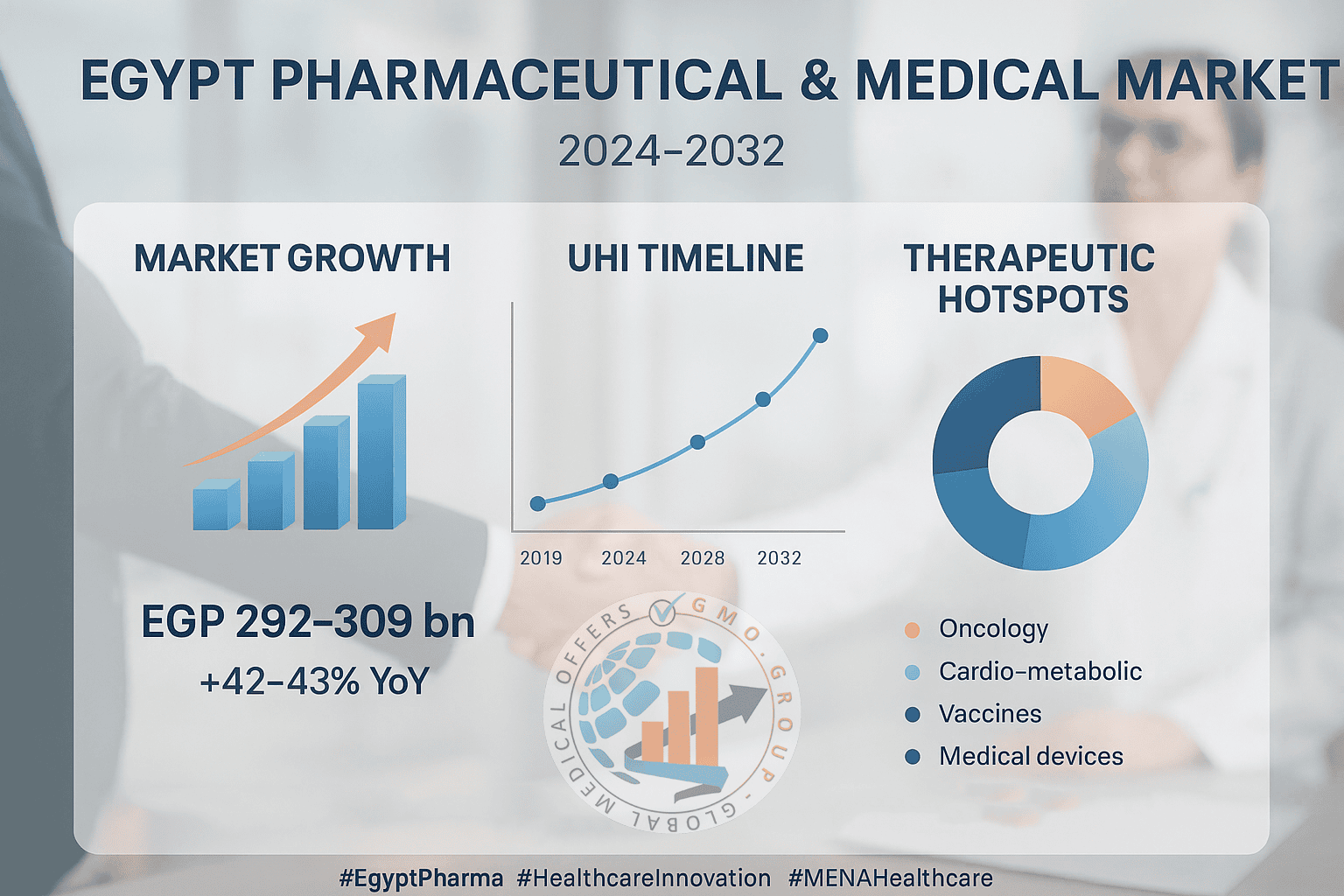

Egypt Pharmaceutical & Medical Market Report 2024–2032

Prepared for healthcare manufacturers, investors, and policy stakeholders

📊 Executive Summary

Egypt’s pharmaceutical and medical market has become one of the fastest growing in MENA, driven by healthcare reforms, rising demand for chronic disease management, and strong localization policies.

-

Market size (2024): EGP 292–309 billion (USD ~9.4 bn).

-

YoY growth: +42–43% vs 2023.

-

Medical devices market (2024): USD 4.3 bn, projected to reach USD 5.6 bn by 2032 (CAGR ~3.3%).

-

Population covered by Universal Health Insurance (UHI): Target 100% by 2032.

🏥 Healthcare Reform & Demand Fundamentals

-

Universal Health Insurance Law (2019–2032): Phased rollout across governorates; separation of payer/provider; standard benefit package.

-

Law 87/2024 (Private Sector Participation): Expands private operators’ role in running public facilities.

-

Population drivers: >110 million citizens, rising chronic disease burden (cardio-metabolic, oncology, endocrine).

📈 Market Dynamics

-

Retail channel dominance: ~70% of sales, but institutional share rising with UHI adoption.

-

Volume sold (2024): 3.5 billion packs, across >12,000 registered products.

-

Currency & inflation impact: Growth is price-led, driven by portfolio repricing in H2 2024.

⚖ Regulatory Transformation – Egyptian Drug Authority (EDA)

-

Biologicals registration guideline (2024, V3).

-

Biosimilar guideline (2024 update): Aligned with ICH, enabling faster approvals.

-

Digitized submission (2024): Streamlined marketing authorization workflow.

Impact: Clearer technical pathways, faster approval cycles, competitive edge for CTD-ready dossiers.

💊 Therapeutic & Product Hotspots

-

Oncology & Biosimilars: Growing demand under UHI tenders and private oncology centers.

-

Cardio-metabolic & Endocrine: High chronic disease burden = sustained demand.

-

Vaccines & Injectables: Priority for localization and regional exports.

-

Medical Devices & Diagnostics: Strong demand in imaging, IVD, and point-of-care diagnostics.

🌍 Export & Regional Outlook

-

Egypt positioning itself as a manufacturing and packaging hub for Africa and MENA.

-

Government-backed incentives for tech-transfer, toll manufacturing, and exports.

-

Rising opportunities in secondary packaging and fill & finish for GCC/EU supply.

⚙ Key Challenges & Risks

-

Currency devaluation & inflation → heavy dependence on imported APIs.

-

Supply chain volatility → strategic push for localization.

-

Tender pricing pressure → necessity of pharmaco-economics and value-based contracts.

✅ Strategic Recommendations for Manufacturers

-

Portfolio Design: Focus on oncology, biosimilars, and chronic therapies.

-

Market Access: Hybrid retail + institutional approach aligned with UHI.

-

Regulatory Readiness: Invest in comparability studies & CTD dossiers for accelerated approvals.

-

Localization: Explore tech-transfer & contract manufacturing for tender eligibility and FX protection.

-

Devices: Target diagnostics & imaging aligned with UHI facility upgrades.

🤝 How Global Medical Offers (GMO Group) Enables Growth

-

Market Entry: EDA-compliant regulatory execution & fast-track pathways.

-

Channel Access: Partnerships with top wholesalers and institutional buyers.

-

Tender Navigation: Expertise in UHI tenders, pharmaco-economics, and pricing strategy.

-

Localization Support: Matchmaking for tech-transfer and regional exports.

🔖 Suggested Hashtags for Corporate Positioning

#EgyptPharma #HealthcareInnovation #Biopharma #MENAHealthcare #MarketAccess #MedicalDevices #Oncology

📚 References

-

IQVIA / Ibnsina Pharma – Market insights (2024).

-

Egyptian Drug Authority (EDA) – Registration Guidelines 2024.

-

Universal Health Insurance Authority (UHIA) – Reform Roadmap (2019–2032).

-

Ministry of Health and Population – National Health Strategy 2024–2030.

-

Business Monitor International (BMI), Fitch Solutions – Egypt Medical Devices Market Forecast.